On June 20th, RBI issued a direction disallowing non-banking Prepaid Payment Instruments (PPI) from loading credit lines on the PPI. This bans PPI wallets from being loaded with credit lines/credit cards.

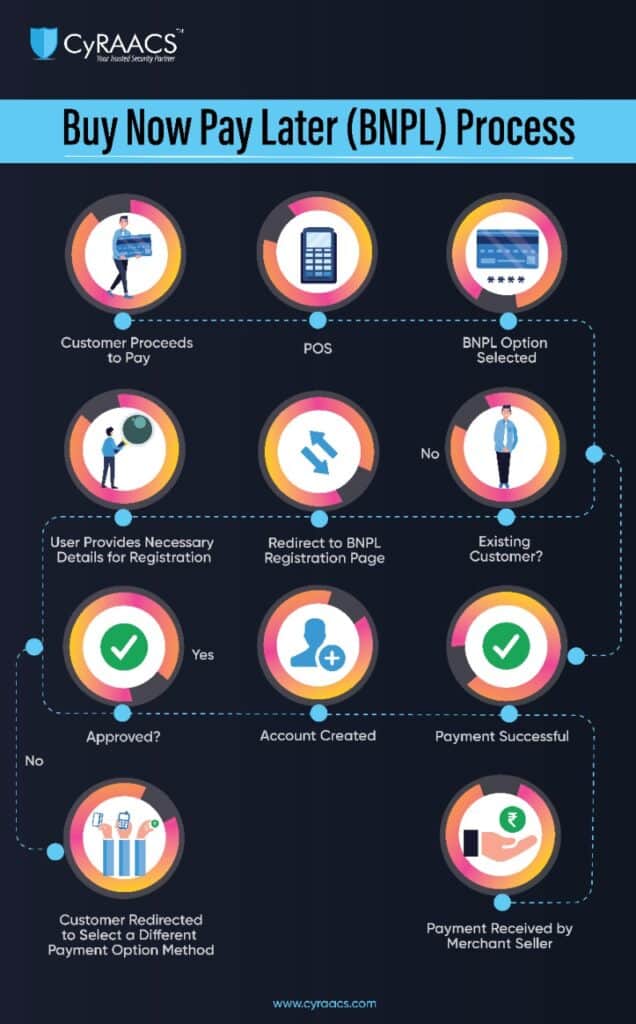

BNPL is short-term financing for consumers who can buy products and get short-term credit and pay later for the credit taken. Well, isn’t that what credit cards are used for as well? The concept of BNPL is similar to that of credit cards wherein a consumer makes a purchase through a credit line and the payment is done later- quite literally “Buy Now, Pay Later”. The BNPL market has grown a massive 539% in 2020 and 637% in 2021.

Credit Cards are given to individuals with a minimum average income of INR 1-3 lakh per annum. Eligibility for a credit card is based on multiple parameters age, salary (ability to repay), type of employment, and credit score. RBI has definite directions for the issuance and operations of credit cards.

There aren’t instruments to finance instant loans without an elaborate process. This is where BNPL comes in. Unlike for credit cards, BNPL issuers do not require credit score and other stringent checks prior to onboarding. This makes credit more accessible. While cursory checks are being done on the spending pattern of customers, it taps on the customer’s ability of immediate spending.

Another difference is that credit cards require a joining and/or an annual fee, while BNPL cards do not levy any such charges/hidden charges on the consumers. That means that all is great if consumers pay their bills on time, however, failing so, the issuer will charge a delay fee. Additionally, the BNPL service is fast and easy to set up as the approvals are almost instant and offer easy repayment options with EMI.

In the past month, the number of credit cards issued was recorded as 15 Lakh, while 20 Lakh BNPL accounts have been opened. This jump seen in the BNPL market made the traditional credit card issuers jittery. The credit card market is currently operated by major banks in the country.

While all seemed to be a fairy tale and a bed of roses for consumers and BNPL entities with heavy investments flowing into the market, the Reserve Bank of India (RBI) threw a bombshell that may have put BNPL entities in the backfoot. The RBI notification restricts non-banking Prepaid Payment Instruments (PPI) from loading credit lines on the PPI. This bans PPI wallets from being loaded with credit lines/credit cards through financing done by NBFCs.

Most popular BNPL players operate using banks’ license/banks’ NBFC license. Alternatively, banks hold PPI license. On the PPI wallet, a credit line was given which was not in line with the PPI directions from RBI.

The main concern that RBI has raised is the lack of clear guidelines/regulations around BNPL. The main focus with which RBI has been operating in the protection of consumers. While consumers seem to be enjoying it, BNPL as a business does not seem viable unless properly regulated over and above the credit card market.

Unlike concerns raised by some on RBI’s stand, the regulatory body has indeed mentioned BNPL in their

“Payment Vision 2025” was released in June 2022. As per the vision document,

BNPL should be:

The Current Market: Its Ups and Downs

Quite a positive right?

But here’s the catch! BNPL is risky lending and there has been a rising trend of defaults accounting for about 18-19% of delinquencies. One main reason that can be attributed to this trend is the provisioning of BNPL cards to Millennials and GenZ as several of them are unemployed, are studying, or are employed but do not have the ability to repay (as per stats in the US BNPL market). This in turn creates a debt trap for consumers as they tend to pay back the existing loans with further credit lines, while the expenses continue to pile up. India is a savings-based economy, contrary to other countries such as the USA, which is credit based.

On the contrary, below are the downsides of BNPL:

The business model is quite ambiguous for BNPL players. Also, as mentioned above, there isn’t a mechanism in place currently to link BNPL defaults to the credit score. Above this, BNPLs adopting AML and Fraud Risk mechanisms within their system is not transparent.

BNPL Stats across the Globe

Recently, OpenPay, a BNPL company in Australia paused operations in the USA due to defaults and rising interest rates. Klarna, another fintech in BNPL has lost its valuation from $45 Billion to $6.5 Billion in the last round of funding and another Australian BNPL firm has lost its valuation to $300 Million from $9 Billion.

Fintechs and BNPLs shouldn’t worry yet as it’s a wait-a-watch game with RBI. The aura in the market is that the central bank will issue new guidelines for the BNPL segment that will not only regulate the sector but also reshape it all together with a focus on consumer protection, risk management, and overall security.

The Indian Fintech and BNPL spaces are nascent and not very mature. The regulator has put in some basic controls at this point in time to ensure that the consumer is not affected by a debt trap, at the same time realizing that for having a spending economy, these kinds of instruments are necessary. The balance may tilt from one side to another every now and then, but at this point, we are poised for some more interesting creative fintech instruments coming in with the regulator constantly on the catching-up game.